Raising your Seed Round 101

Who To Approach?

First thought of the day should be whether or not your business is a fit for VC money. As this subject is covered extensively in various blogs we can skip it (I recommend 1 & 2).

Second thought is “Which VC is right for me?”. Entrepreneurs often do not think about this question enough, which results in a meeting ending before it has even begun.

There are some obvious questions each founder should ask before she/he begins fundraising:

- Are they invested in my direct competitors? (If they are, might not be the best idea to approach)

- Do they know my industry? (If they do, the pitch will be easier as they understand your surroundings and can jump to the tough questions quickly (Tip: Look at the partners’ history, companies they were involved in).

3. Do they invest in my stage? (Is the check I am asking for the check they can write?)

Apart from these there are other crucial questions entrepreneurs must ask:

- What is the fund size?

Why is this important? If the latest fund this VC is deploying from is a $2bn fund and your Total Addressable Market is $200mm there is little chance a deal could be struck here.

2. When was the latest fund raised?

VCs typically invest 2–4 years max from the moment the fund starts investing. If the VC raised it’s last fund 7 years ago and has not raised since you are probably wasting your time approaching them as they have no money to invest in new ventures, only to follow on on their existing portfolio.

Dirty secret: they might still meet with you just to learn about your tech and/or space but will not invest as they cannot.

A smart question can be “How much of your fund have you deployed already?”. That way you can understand how much money they have left for new investments.

Bottom Line: Make sure the VC has the ability and strategy to write checks in the size you seek, in your industry.

How To Approach?

Now that you know which VCs you want to target, the question arises: “How do I reach out to them?”.

The best approach on a scale from best to worst:

- Nothing beats inbound — if you have a person close to the GP which can whisper in his ear that you are doing really well and he should meet you, that puts him “on the chase”, and you in a great position.

- Get a warm intro.

A) Best intro is from an entrepreneur who has exited with the fund or strong entrepreneurs who have worked with the fund / GPs before.

B) Smart successful people of whom the GP might think highly.

C) A VC which thinks your venture is potentially great but does not have the mandate to do the deal (different stage, industry).

D) Lawyers sometimes send startups to VCs as an extra service to their startup clients, good lawyers send good deal flow.

E) Accountant firms send deal flow which can be outdated. The reason for this is that they see the companies in a later stage (after there is a company, employees, revenues etc.) so they might send your deck to VCs you have seen months ago (which does not look very good).

When sending the first email, be sure to make it personal, obviously state the name of the partner but, also dedicate a line or two about why you are approaching them, (example: “I saw your investments in Riskified & Fundbox and as our venture is in Fintech I think there can be a great fit here”)

Bottom Line: try to manufacture inbound or get a warm intro by a person whom the partner will think highly.

What are VCs after?

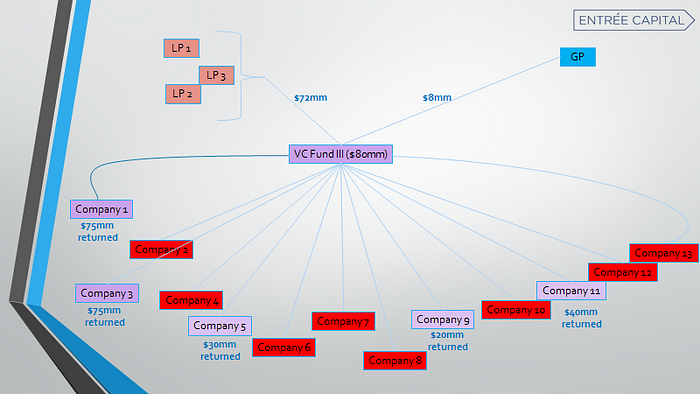

1. VCs are structures which contain LP’s (those who invest money) and GP’s (those who manage said money and invest a small %). Since VC is a highly risky illiquid investment vehicle (especially for Seed) the LP’s expect that by the time the fund is done (~10 years) they will get at least 3X on their money (This is a generalization in order to keep it simple).

The above returns force a $80mm Seed fund to return about $240mm back to their investors. Assuming they do $3mm investments and keep a 1:1 ratio of reserves for follow on’s excluding fees they will make roughly 13 investments. Early stage Startup’s usually fail. That’s just a fact of life. If the VC wants to return $240mm they need to have let’s say 2 winners which exit at a $500mm valuation, in which the VC still held 15%.

Couple those 2 X $75mm returns with 2–3 others which returned 5x-7x and you can reach the $240mm mark. Notice 2–5 companies out of 13 are the major value drivers of the fund, whilst the rest either turned to 0 or returned a 1x-2x. The above is covered extensively by some great sources, I like this one.

2. The above math creates a situation in which the VC MUST take big bets to be successful in his business. So if you are targeting a $500mm market, if you have no company which is likely to acquire you or if you cannot grow from 0 to tens of millions in revenue in 5 years you will have a problem raising VC dollars. You can say, “but not all their investments must be unicorns, what if I can exit for $50mm but raise only $3mm? Is that not good enough?. No. (even with a 25% stake, $50mm exit is only $12.5mm which does not move the needle for even a $80mm fund).

The VC does not know which of the 13 will be a home run so he must make sure each of his bets are at least capable (in theory) to reach these numbers, if he invests too much in startups in tiny markets there is no way he can get the needed return for his LP’s.

What To Prepare?

- A 2–3 line paragraph which explains your venture perfectly

- Executive summary, A.K.A one pager

- Deck (I recommend a short deck for emails and long deck for face-to-face presentations)

- TAM Analysis — market size both bottom up and top down

- Competitive analysis — all of your (or main if there are too many) direct and indirect competitors, coupled with their key metrics and explanation of why you are different

- Budget — sometimes known as business plan, this Excel should be able to explain what you are going to spend the money on and what revenue / key KPI’s will be reached and when.

- Go To Market Strategy — a short document explaining exactly how you plan to acquire your customers at scale.

- Current metrics, clearly presented — if you have traction, use it!

- Legal docs — COI, founders agreement, Cap table and anything else needed if you have a history (if you have not even opened a company these can be done during the round).

How do you rate on the “Scorecard”?

VCs look at many things to evaluate a potential investment and there are many online guides, to break it down (I highly recommend this one), this list encompasses the key components all VCs look for:

- Team — Especially in the Seed stage, it’s all about the team. Can the CEO run a company? Do they have the tech skills to build their vision? Are they the best out there at tackling this problem?Do they have any experience in the industry they are tackling?

- Problem — Is it a real problem? Is your product a “must have” for your target customers?

- Tech — Is it a major success factor? Can it create a moat which defends from competition?

- Market — How big is the market? How fast is it growing? Are there giants dominating the space? Is the market fragmented?

- Competition — how many are there, what size, how do you differentiate? how will you beat them?

- Go To Market — How do you get your product in customer hands? Who are you targeting? What are your distribution channels?

- Execution — What have you got today? How long did it take you to get there? What are your metrics? Have you validated your solution with the market?

- Finance — Fundraising history, if it exists,the next milestones for fundraising. Essentially, where does this round take you and will it be enough to raise the next round?

Bottom Line: VCs back talented entrepreneurs who are going after painful problems, in big markets, and can become the leader in their category.

The Bottom Line

Raising your Seed round is not an easy process and if you are not an experienced founder it may take you a few months to complete. Raising funds is a task which requires planning and strategy.

Be sure to prepare a list of all the VCs you want to target, get a great intro, prepare your materials, and have your pitch ready.

Best scenario for you is to create competition between VCs, which will result in a few term sheets. This will drive up the amount of money you can raise and the valuation as well.

Good luck!

Related Resources

The Rise of Mission-Driven Founders: Beyond Profit to Purpose